How to offset the rising cost of your child's education in Singapore

The average cost of education in Singapore has risen by as much as 75.7 per cent in the past two decades and it will continue to grow in an upward trend alongside the escalating cost of living. If you are a new parent, this is probably a red alert to start saving early for your child's future tertiary education.

How much savings is enough? Let's take a closer look at past statistics to help you anticipate the education expenses you can expect to pay.

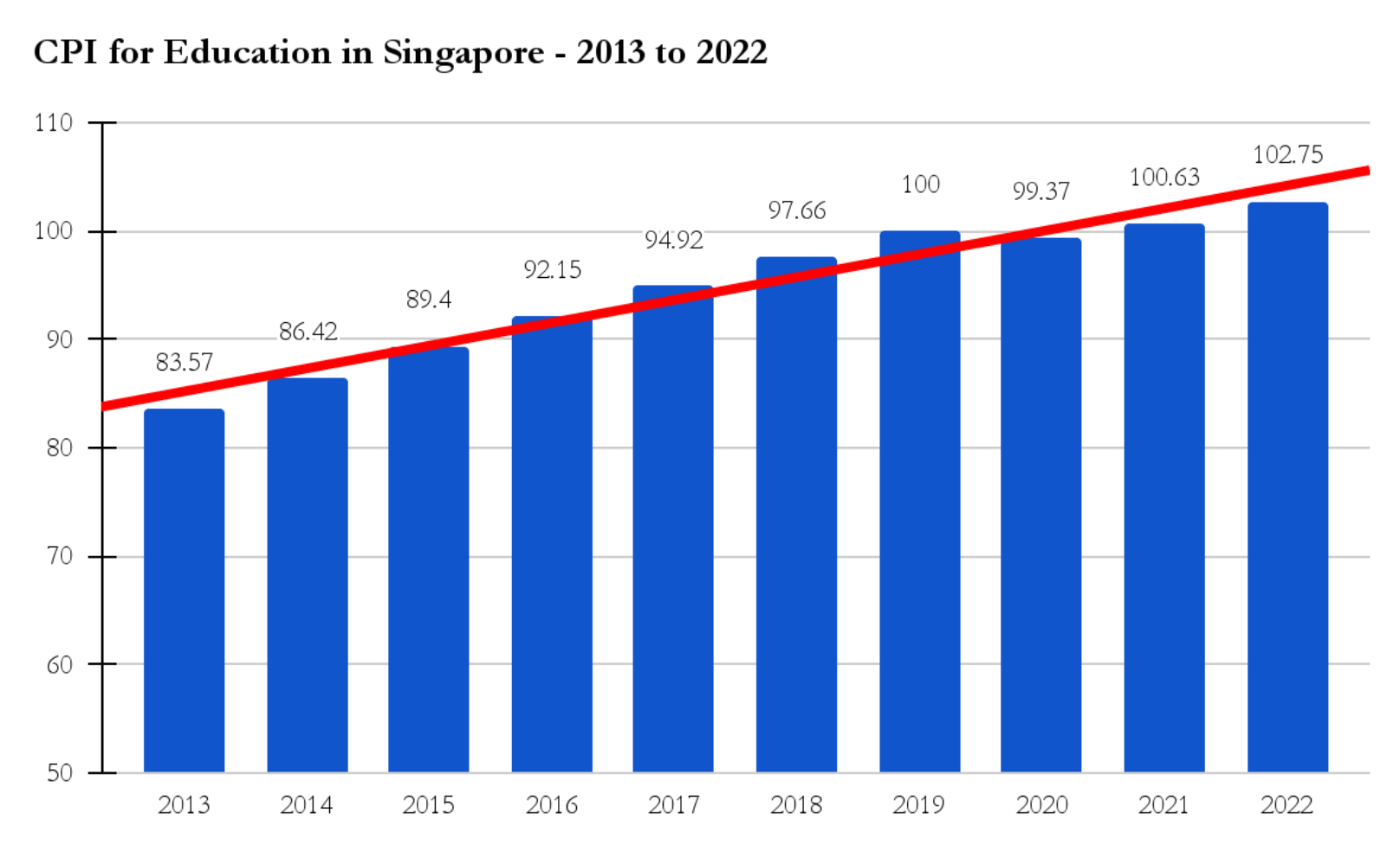

Real statistics on the rising cost of education in SingaporeA quick glance at the Consumer Price Index (CPI) on education in Singapore from 2013 to 2022 would predict that the rising cost of education will continue its upward trajectory in the future.

Reportedly, the figure for October 2023 has already reached 106.04, an increase of 3.29 over the previous year, also the highest change recorded in the past decade. Based on this figure, education expenses that were S$10,000 in 2013 would have increased by 26.89 per cent to S$12,689 by now.

There are multiple reasons for the increase in the average cost of education in Singapore — cost of living, increased wage and technological advancements of facilities and infrastructure all count as factors that significantly impacted overall cost.

Singapore's renowned positioning as a global education hub also contributes to institutions raising their fees and services to compete more aggressively with international institutions to attract local and overseas students.

Ways to plan for your child's educationThe first step is to determine how much your child's education needs. Assuming your child is a Singapore citizen, the estimated average cost of education in Singapore is close to S$70,000. This is based on local education and government school rates.

Average Cost of Education in Singapore Full-day infant care – 16 months S$10,141 (after subsidies with the median household income) Full-day child care - 66 months S$20,090 (after subsidies with the median household income) Primary school – 6 years S$936 Secondary School – 4 years S$1,200 Junior College – 2 years S$792 University – 4 years S$38,250 Source: Smart WealthIf an undergraduate education abroad is what you intend for your child, the following are estimates that will be helpful for your financial planning.

Once you work out how much is required to fund your child's education and the time frame you have to save up this amount, be sure to factor in an annual education inflation rate of 2.86 per cent. This is a close estimated percentage based on figures collected over the past 20 years. Not sure how to tabulate? Try using online education inflation calculators. They are relatively easy to use.

The next step is to develop a strategy to grow the funds you have on hand. Most parents will not have their children's education fund right from the get-go but you can certainly grow it by investing wisely or saving in bank accounts that let you earn the most interest.

Another straightforward method is to apply for education loans, grants, subsidies, scholarships or bursaries in Singapore to fund your child's education. Here's a quick look at these options.

Types of education loans in Singapore Bank loansMajor banks in Singapore like OCBC, CIMB Bank and POSB offer education loans but they are usually more expensive than government schemes.

The average interest rate for such loans is around 5.46 per cent per annum with 2.15 per cent of processing fee. The loan sum varies between banks. Depending on your eligibility, the maximum loan limit for POSB is S$80,000, CIMB is S$200,000 and OCBC is S$150,000.

CPF education loan schemeThis loan is applicable only if your child is signing up for full-time subsidised diploma or degree courses at Approved Educational Institutions (AEIs). The loan sum is limited to 40 per cent of your savings in your CPF Ordinary Account (OA) or remaining OA balance after setting aside any amounts reserved for housing or other schemes (if any).

For example, if you are 55 years old or above, you need to set aside the Full Retirement Sum (FRS) in the Retirement Account before you can use the remaining savings in the OA for the scheme.

If your child is going to an Institute of Technical Education (ITE), a polytechnic or an autonomous university, you can apply for this Tuition Fee Loan to cover up to 90per cent of the tuition fee. No interest will be charged during the course of the study and there is no need to make repayment until one year after graduation.

The chargeable interest rates after graduation will be according to an average prime rate of participating banks like DBS, OCBC, and UOB.

Subsidies, scholarships and bursaries Government subsidiesThere is a variety of government subsidies available to students from preschool to secondary level. Some of these schemes even cover over 90 per cent of the cost of education for Singapore Citizens.

Level Subsidies Criteria Preschool Infant care subsidies – Up to S$600 per month with additional subsidy of up to S$710Child care subsidies – Up to S$300 per month with additional subsidy of up to S$467

Mother or father must work at least 56 hours per monthChild must be a Singaporean enrolled in an infant or child care centre licensed by Early Childhood Development Agency (ECDA)

Preschool Basic subsidy of S$150 for infant care and child care Applicants are not working or non-parent caregiversChild must be a Singaporean enrolled in an infant or child care centre licensed by ECDA

Preschool Kindergarten subsidies – Up to S$415 per month Family’s gross monthly household income is S$12,000 and belowChild must be a Singaporean enrolled in a Anchor Operator Kindergarten or MOE Kindergarten

Primary and Secondary Student Care Fee Assistance - Up to S$290 Mother or father must work at least 56 hours per month or monthly household income of less than or equal to S$4,500Child must be a Singaporean attending Ministry of Social and Family Development-registered Student Care Centre

Source: Support Go Where, ECDA Government bursariesBursaries are available to Singaporean students with gross monthly household income of up to S$10,000. Families with lower income may get more financial support.

The maximum bursary tiers are as follow:

Full-time and higher Nitec students 100per cent tuition fee and annual cash bursary of S$1,600(Annual tuition fee is S$430 to S$590)

Full-time Diploma students 95per cent tuition fee(Annual tuition fee is S$3,000)

Full-time undergraduates 75per cent tuition fee(Annual tuition fee is S$8,250)

Source: MOE ScholarshipsGetting a scholarship is extremely helpful for reducing education costs and ensuring job security after graduation. However, most scholarships do come with a bond that locks the graduate in an employment contract of one to 12 years. If that sounds too restricting, try looking for bond-free scholarships instead.

Do note that scholarships are only given to students with outstanding achievement. If you want your child to get a scholarship that frees you from paying large education costs in Singapore, you have to make sure he or she is putting in the effort to get top grades.

ConclusionIt is never too early to start financial planning for your child's future. If you need assistance to shortlist the best education loans in Singapore, our research team has analysed hundreds of loan packages to identify the most affordable one that is based on your preference.

ALSO READ: School fees to rise for PR and foreign students in government-funded schools: MOE

This article was first published in ValueChampion.